Navigating Student Debt

- Nov 4, 2025

- 6 min read

Student loans have become an unavoidable reality for millions of Americans pursuing higher education. While borrowing for college can feel overwhelming, understanding the basics and having a solid management strategy can help you take control of your debt and set yourself up for financial success after graduation.

Before You Borrow: Exhaust Your Free Money Options First

The most important rule of student borrowing is deceptively simple: don't borrow what you don't need to. Before signing on the dotted line for any student loan, make sure you've thoroughly researched and applied for all sources of free financial aid. This includes scholarships, grants, and work-study programs. Unlike loans, these forms of aid don't need to be repaid, making them infinitely more valuable to your long-term financial health.

Start by completing the FAFSA (Free Application for Federal Student Aid) to determine your eligibility for federal grants and work-study. Then cast a wide net for scholarships—look beyond the big-name national competitions to local organizations, your intended major's professional associations, and your parents' employers. Even small scholarships of a few hundred dollars add up and reduce your borrowing needs.

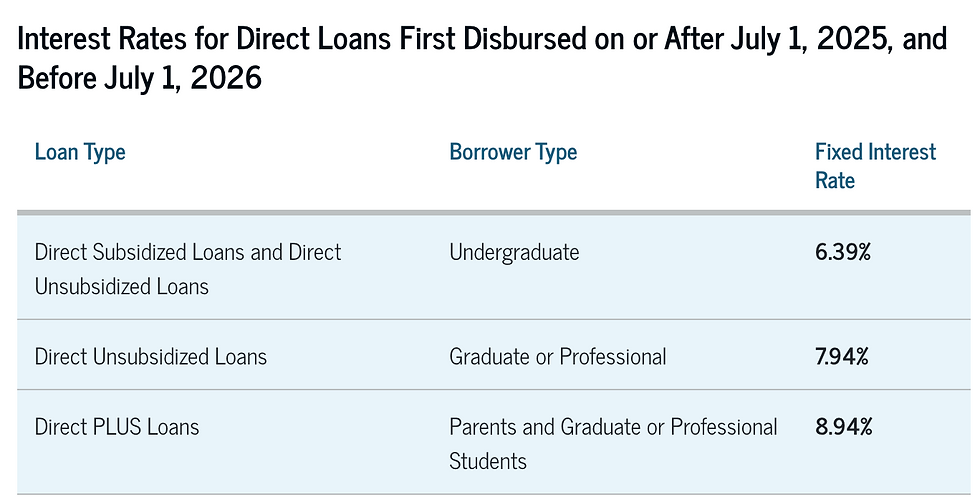

Comparing Your Loan Options: Federal First, Private Last

Once you've maximized your free aid, it's time to understand your borrowing options. Not all student loans are created equal, and the type of loan you choose can significantly impact your repayment experience.

Federal student loans should always be your first choice. These loans, backed by the U.S. government, offer crucial protections and flexibility that private loans simply don't provide. Federal loans come with fixed interest rates, income-driven repayment options, deferment and forbearance opportunities, and potential loan forgiveness programs for those working in public service or other qualifying fields.

Private or alternative loans from banks, credit unions, or other lenders should only be considered as a last resort after you've exhausted federal loan options. These loans often have variable interest rates, require credit checks, may need a cosigner, and lack the borrower protections that federal loans provide.

Take the time to compare all available loan programs carefully. Understand the interest rates, repayment terms, and borrower benefits before making your final decision. Different federal loan types (Direct Subsidized, Direct Unsubsidized, Direct PLUS) serve different purposes and have different eligibility requirements. Be sure to use a Loan Comparison calculator to help determine what loan is best for you.

Understanding Your Loans: Knowledge Is Power

Many students sign their loan documents without fully grasping what they're agreeing to. This lack of understanding can lead to problems down the road. Make it a priority to know the details of your loans: Who is your loan servicer? What type of loan do you have? What is your interest rate? When does repayment begin?

Your loan servicer is the company that handles the billing and other services on your loan. This may not be the same entity that originally provided your loan. Keep track of your servicer's contact information and don't hesitate to reach out with questions. They're there to help you navigate the repayment process.

Understanding what having a student loan really means also includes knowing your rights and responsibilities as a borrower. You're expected to make timely payments once your grace period ends, keep your contact information current, and notify your servicer of any changes that might affect your ability to repay.

Budget Before You Borrow: Plan for Both Now and Later

One of the biggest mistakes students make is borrowing without a realistic budget. Before you take out your first student loan, create both an in-school budget and an after-school budget. Your in-school budget helps you determine exactly how much you need to borrow to cover tuition, fees, books, housing, and reasonable living expenses. Your after-school budget helps you understand what your financial life will look like once you graduate and enter repayment.

Determine how much you can realistically afford to borrow based on your expected career earnings. A common rule of thumb suggests that your total student loan debt should not exceed your expected first-year salary. Research typical starting salaries in your intended field and use that information to guide your borrowing decisions.

Before committing to a loan amount, estimate your monthly student loan payment using online calculators. This exercise brings abstract future obligations into sharp focus. Seeing that you'll owe $400 or $600 or $1,000 per month after graduation can be a powerful reality check that influences your borrowing decisions today.

Starting Repayment: When and How

Understanding when to start paying your lender is crucial. While you can begin making payments anytime—even while you're still in school—most federal student loans come with a grace period after you graduate, leave school, or drop below half-time enrollment. This grace period, typically six months, gives you time to get financially settled before mandatory payments begin.

However, interest on unsubsidized loans continues to accrue during this grace period. If you can afford to make interest-only payments during school or during your grace period, you'll save money in the long run by preventing that interest from capitalizing (being added to your principal balance).

Once your grace period ends, you must start making payments. Missing payments can damage your credit score and lead to default, which carries serious consequences including wage garnishment, tax refund seizure, and loss of eligibility for deferment, forbearance, and additional federal student aid.

Choosing Your Repayment Plan

The federal student loan program offers multiple repayment options, giving you flexibility to choose a plan that fits your financial situation. The Standard Repayment Plan spreads your payments over 10 years with fixed monthly amounts. This plan typically costs you the least in interest over time but requires higher monthly payments.

Income-driven repayment plans adjust your monthly payment based on your income and family size. These plans extend the repayment period to 20 or 25 years and can result in loan forgiveness at the end of the term. While income-driven plans offer lower monthly payments that adjust as your income changes, you'll typically pay more in interest over the life of the loan.

Don't feel locked into your initial repayment plan choice. If your financial situation changes, you can switch to a different repayment plan. Contact your loan servicer to discuss your options and determine which plan makes the most sense for your current circumstances.

When Life Happens: Deferment, Forbearance, and Consolidation

Even with the best planning, life sometimes throws curveballs that affect your ability to make your student loan payments. If you're facing temporary financial hardship, unemployment, or other qualifying circumstances, you may be eligible for deferment or forbearance, which allow you to temporarily suspend or reduce your payments.

Deferment is preferable when available because the government may pay the interest on subsidized loans during the deferment period. With forbearance, interest continues to accrue on all loans. Both options provide breathing room, but should be used thoughtfully as they extend your repayment timeline and can increase your total cost.

If you're juggling multiple federal student loans, a Direct Consolidation Loan allows you to combine them into a single loan with one monthly payment. This can simplify your repayment and may give you access to alternative repayment plans. However, consolidation can also result in losing certain borrower benefits and may increase the total interest you pay if you extend your repayment term.

Special Circumstances: Forgiveness and Cancellation

Your career path might make you eligible for loan forgiveness programs. Public Service Loan Forgiveness (PSLF) forgives the remaining balance on Direct Loans after you've made 120 qualifying monthly payments while working full-time for a qualifying government or nonprofit organization. Teacher Loan Forgiveness programs offer forgiveness for teachers who work in low-income schools or educational service agencies.

Members of the U.S. military may also qualify for various loan forgiveness or repayment assistance programs. In rare cases involving school closure, false certification, or fraud, federal student loans can be canceled completely.

Building Your Credit Future

Student loans represent many borrowers' first experience with credit, making them an opportunity to establish a positive credit history. Consistently making your student loan payments on time demonstrates financial responsibility to future lenders and helps build a strong credit score. This credit history will benefit you when you apply for a mortgage, car loan, or credit card down the road.

Conversely, late or missed payments damage your credit and can haunt you for years. Treat your student loan payment as seriously as you would rent or a car payment—it's a non-negotiable monthly obligation.

Additional resources: